Value investing is hard to define.Not that the meaning of “value” is elusive. It’s not. More because defining what’s actually valuable in the market is difficult.This might surprise anyone who thinks they’re a value investor because they buy stocks with a low price-to-earnings (P/E) ratio. That’s a popular — but inadequate — way to look for value.The problem with buying “low-P/E stocks” is what “low” actually means. Some investors say a P/E of 15 is low. Others want 12, or … some other number.But a simple number won’t ever beat the market. To do that, you need to analyze value in context. You need to understand a stock’s relative value, not just its absolute value. And to do that, you need to look at more than one number.That’s a lot of work, which is why so few people do it. Luckily, because you’re reading this, you don’t have to.I’ve done a lot of relative value analysis over the decades. It’s always pointed me toward stocks and sectors that are poised to beat the market in both good times and bad.I’ve run the numbers once again. And it’s telling me just one sector presents the golden crossover of value and growth to make it an attractive investment for 2023. So much so, it’s practically the only place a value investor should look.Read on to learn which sector will be the only one a value investor can stomach in 2023, and the best way for you to get involved right now…

[Whitney Tilson: Gold 2.0 Tap Into the Most Lucrative Vein of the SWaB Revolution]

STILL CHEAP ON 3 DIFFERENT METRICS

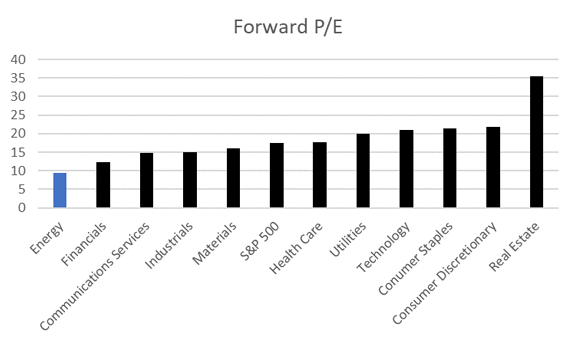

For my money, you shouldn’t just use the standard P/E ratio to measure value. You should, at the very least, also use the forward P/E ratio.The forward P/E ratio uses expected earnings, where the standard P/E ratio uses earnings from the past 12 months. In other words, it’s backward-looking, and therefore not much help in making investment decisions.Buyers expect the stock to move up because of future earnings, not past earnings. Sellers expect the future to be less enticing than the past. So, using expected (forward) earnings aligns the P/E ratio with the actions of current buyers and sellers — who ultimately move the market.With that in mind, here’s a look at the forward P/E ratio of every sector in the S&P 500.

Source: banyanhill.com

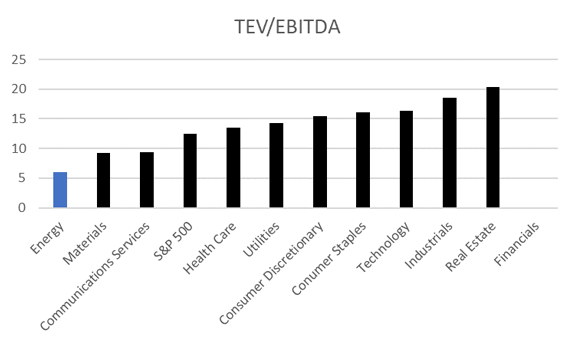

Energy has the lowest forward P/E than any other sector. That tells us 12 months from now, and even after rising 50% in 2022, energy stocks are expected to have the best value.Using forward earnings corrects one problem with the P/E ratio. But there’s no escaping the second problem: the fact that management manipulates earnings.The word “manipulates” sounds nefarious, but it’s just part of the process. All companies who report earnings have to make assumptions about expenses. Many have to make assumptions about revenue. And every assumption affects earnings numbers.Aggressive management teams make earnings look better with some assumptions. Meanwhile, conservative managers understate earnings. They do this to make sure they’re reporting accurate earnings, or alluring earnings, or often some combination of the two.The result is that earnings are never quite what companies say they are.Individual investors might ignore all this, but investment bankers don’t. That’s why they use another valuation metric called Total Enterprise Value to Earnings Before Interest, Taxes, Depreciation and Amortization, or TEV/EBITDA.TEV accounts for all of a company’s debt and equity. EBITDA factors out many assumptions. Put them together and you have a much more comprehensive look at a company’s valuation. That’s why mergers and acquisitions — some of the most important dealmaking that occurs in markets — rely on TEV/EBITDA calculations.Here again, energy holds the highest value in the S&P 500, according to its TEV/EBITDA.

Source: bayanhill.com

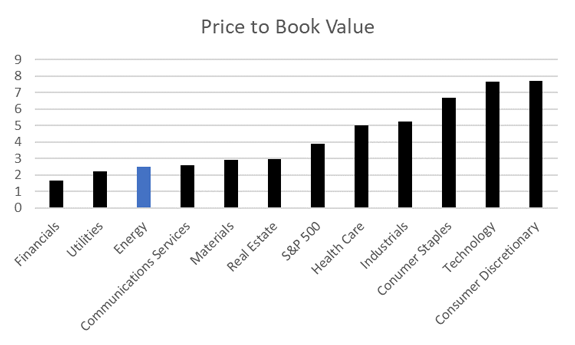

(Note: There is no TEV/EBITDA metric for the financials sector. Debt carries a different meaning for banks than a company providing goods or nonfinancial services. TEV also doesn’t mean the same thing in that context. So that column is blank.)The low TEV/EBITDA indicates we may see a lot of M&A activity in the energy sector. More mergers and acquisitions means more investment interest in the energy space, which is naturally bullish for energy.Then there’s one last important fundamental metric — the price-to-book value (P/B). Book value is a conservative measure of a company’s value. Here again, energy is near the bottom of the list, indicating a high degree of relative value.

Source: bayanhill.com

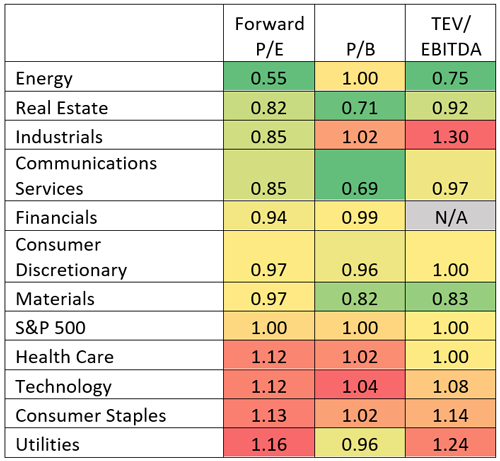

These charts all show energy is undervalued. That’s relative to other sectors and the broader market.But there’s a second, even more effective way to find relative valuations.The last chart I have to share today does that.

[Jim Rickards Asset Emancipation: Profit from the 3 Companies Building “Biden Bucks”]

BRINGING IT ALL TOGETHER

Remember when I said value investing is hard? You’re about to see exactly why.The final chart I want to share today compares the current values of each of the above valuation metrics to its 10-year average. Those values are then compared to the S&P 500.Values less than 1 are undervalued, where values over 1 are overvalued.The color spectrum below indicates where each sector scores on each relative metric. Green indicates a value that’s well under the benchmark, where red indicates a value high above.The chart confirms energy is highly undervalued compared to both its 10-year average and the S&P 500 on two metrics.

Source: banyanhill.com

This is the kind of relative value analysis that helps show the future winners and losers in the market. And we can see clearly that energy shows the best overall value.That means these stocks could deliver strong gains in 2023 no matter what the broad market does.In no shortage of words, you should be invested in energy stocks.Whether you choose to buy the Energy Select Sector ETF (XLE), one of the major companies like Exxon-Mobil (XOM), or a smaller-cap play is entirely up to you.Regards, Michael CarrEditor, One Trade

Michael CarrEditor, One Trade

[Alex Reid: Ride the Future Fuel Revolution for Life-Changing Gains]