The stock market's rise over the last decade has left a lot of companies with dizzying valuations. But there are still stocks that investors can consider a value, whether it's their price to earnings multiple or competitive moat making them cheap to hold long term.

Apple (NASDAQ:AAPL), Intel (NASDAQ:INTC), and Verizon (NYSE:VZ) are all cheap right now based on both their valuation and position in the market. Here's why:

The stock market giant

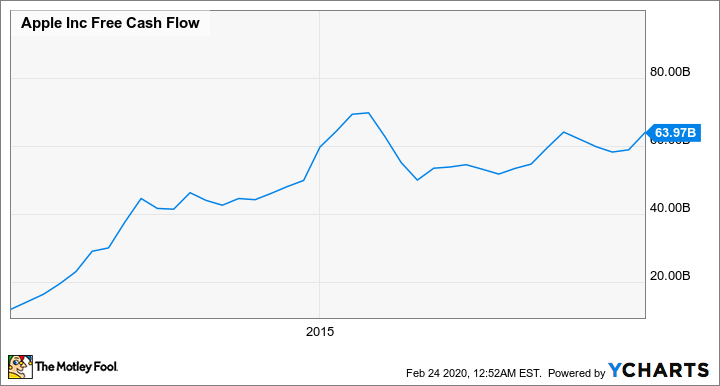

It may seem crazy that one of the most valuable companies in the world is cheap, but that's exactly what Apple stock is today. Shares trade at roughly 20 times trailing free cash flow, and cash flow has grown for more than a decade, as you can see below.

What's amazing about Apple is that it has a nearly indestructible business model in smartphones. The iPhone is its core product and commands a premium price while selling hundreds of millions of units per year. Until a better smartphone ecosystem comes along (which I doubt will happen) or a new technology paradigm begins, the company can count on consistent iPhone cash flow. From there, it will continue to expand into new businesses like AirPods, the Apple Watch, and services. As cash flow grows, so will buybacks and dividends that add to shareholder value. That's why it's a cheap stock today.

[Learn More: The Company About to Blow Nearly Every Other Tech Firm Out of the Water]

The forgotten tech stock

Intel was once one of the hottest technology stocks in the world. But after effectively missing the mobile revolution, it fell out of favor with investors. Now, a resurgence in the PC market and growth in cloud computing have put the company on solid ground once again.

Revenue and free cash flow are both growing once again, and as the data center business grows, the trend should continue. This won't blow away investors with growth, but slow and steady wins the race.

Intel now trades around 14.7 times trailing free cash flow, and I think its business is set up well to grow cash flow. This may not be something you think of as a hot technology stock, but it's a great value and has tailwinds as data centers continue to grow.

[Alert! The Company With Over 200 Patents / 500 More Pending in Tech Called “the new oil.”]

A stock to own in any economy

One business that should be relatively stable even as fear of a coronavirus-induced recession hits the market is Verizon. Mobile phone connections are basically a consumer staple expense at this point, so revenue and earnings should be stable for Verizon no matter the economy.

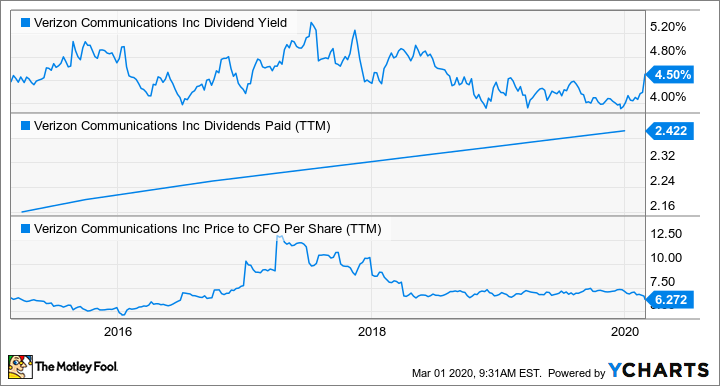

I want to focus on three metrics to show Verizon's value today. The first two are dividends paid, which are growing slowly but surely, and dividend yield, which is now 4.5%. A growing dividend in a consumer staple product is highly attractive in a market where most stocks seem overvalued by the same metrics.

The third metric is the ratio of stock price to operating cash flow per share. At 6.3, Verizon is generating a lot of cash per share. Some of that money then goes back into the business in the form of capital expenditures, but some comes back to shareholders as dividends or share buybacks. As long as cash flow is strong from the wireless business, this should be a great value stock for investors.

[Learn More: The Company About to Blow Nearly Every Other Tech Firm Out of the Water]